Blockchain explained: What blockchain is in simple terms

When it comes to blockchain technology, most people immediately think of Bitcoin and other cryptocurrencies. But the scope of application of blockchain technology is much wider than just cryptocurrencies. Blockchain is considered by many to be one of the most important technologies of the last decade. In this article, we'll explain blockchain in simple terms and answer many popular questions about how blockchain works.

Blockchain's a very interesting technology that will have some very profound applications for society over the years to come. — Kenneth C. Griffin, Founder, CEO, and Co-CIO of Citadel LLC

What is blockchain technology in simple terms?

It can be challenging for people without an IT background to understand what a blockchain is, how it works and what is the main purpose of blockchain. We'll try to explain what blockchain means in simple terms.

The idea behind blockchain technology

What is blockchain and why is it important?

At its core, a blockchain is a method of storing and transferring information. It can be considered a kind of database, albeit one that differs from traditional databases. Information on a blockchain is stored in a continuous chain of blocks, with each block containing essential information (for example, transactions) and the cryptographic hash of the previous block. To change the information in any block, you have to make changes to all subsequent blocks.

A blockchain is also a distributed database, which means it isn't stored on any single computer. Instead, many identical copies of it are stored on a network of different computers called nodes. The content of the blocks is verified by the consensus of all nodes in the network. This makes it very difficult to alter any information already included in the blocks, and this difficulty increases with the number of nodes in the network.

History of its appearance

Who developed blockchain, and when did blockchain come out?

The idea of a blockchain-like protocol was first described in 1982 by cryptographer David Chaum in his dissertation. Later, in 1991, Stuart Haber and W. Scott Stornetta described a cryptographically secure chain of blocks in which no one could tamper with document timestamps. In 1992, they improved their idea to include Merkle trees, which increased efficiency by allowing more documents to be included in a single block.

But the idea of blockchain technology really developed in 2008, thanks to the mysterious creator of Bitcoin, known under the pseudonym Satoshi Nakamoto. On 31 October 2008, a whitepaper on Bitcoin was published entitled Bitcoin: A Peer-to-Peer Electronic Cash System. This whitepaper outlined blockchain technology as we know it now and why blockchain was created. The practical use of blockchain technology started on 3 January 2009, when Satoshi mined the first block of Bitcoin.

First transactions

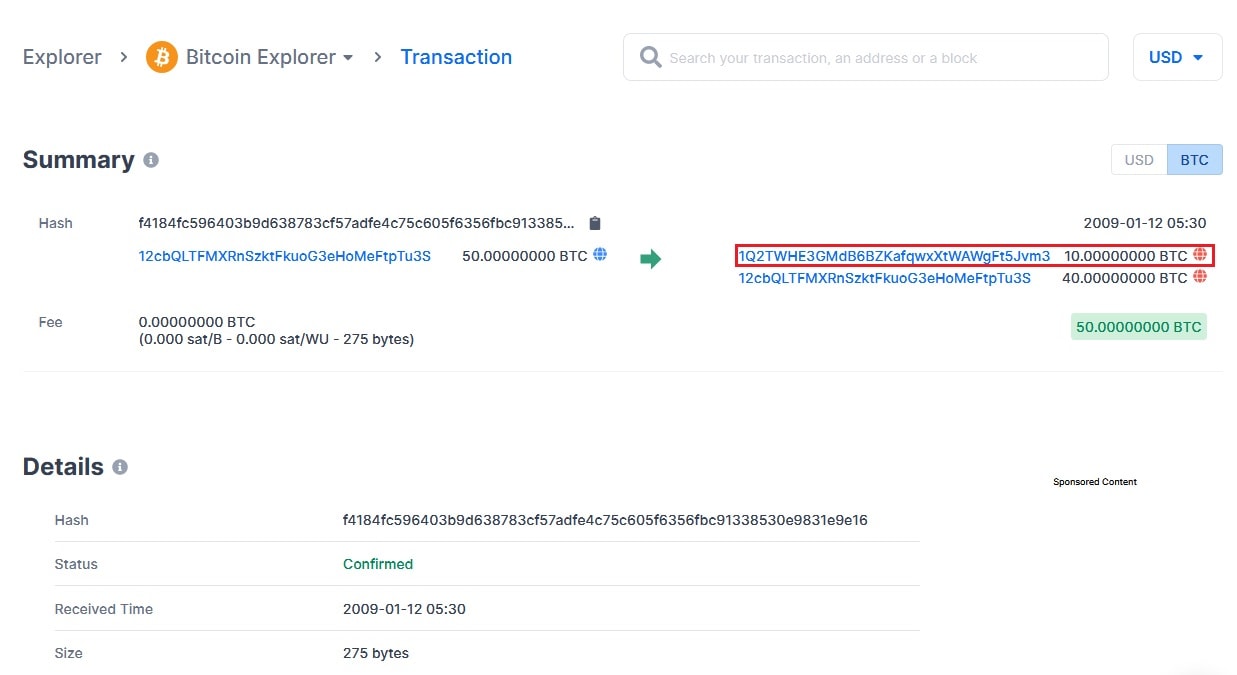

The first transaction via the blockchain was made by Satoshi Nakamoto (i.e., the person who developed blockchain) on 12 January 2009. The recipient of this transaction was Hal Finney, to whom Satoshi sent 10 Bitcoins. On 22 May 2010, the first commercial transaction was made: programmer Laszlo Hanyecz bought two pizzas for 10,000 BTC.

How does blockchain work?

Now, let's explore how blockchain works step by step. Blockchain technology consists of several important elements.

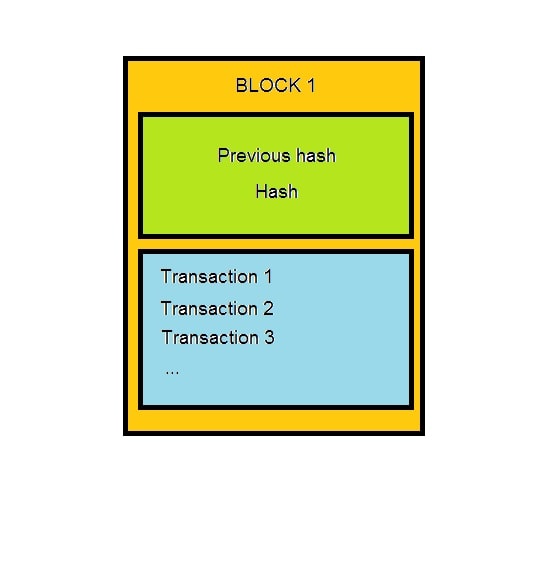

Blocks

The blockchain's fundamental element is a block, and all blocks are sequentially linked into a single chain. Each newly created block contains a group of recently accumulated transactions and information about the previous block. With blockchain, transactions are any actions that blockchain users perform, whether it is sending funds, registering property rights, etc.

When the block is formed, it is verified by other nodes on the network, and then, if everyone agrees, it's connected to the end of the chain. Once this happens, it's no longer possible to make changes to it.

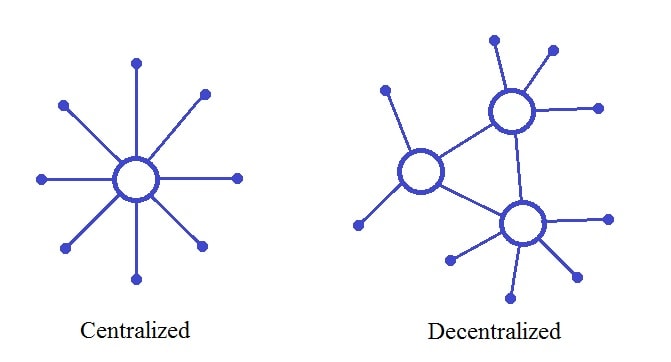

Decentralisation

The blockchain database isn't stored in a single location. Identical copies of it are stored on many computers simultaneously, and its data is available to all network participants. When a new block is added, the database is updated on all nodes in the network. The information in such a database is public and easy to verify. Will blockchain survive if one network node disconnects from the chain or malfunctions? The network's performance won't be affected.

Nodes

A node is an individual computer that stores the complete latest version of the blockchain. When a new block is added to the blockchain, all nodes update their copy of the blockchain.

Cryptographic keys

The use of encryption ensures that users can only modify the blockchain parts for which they have private keys. Transactions are impossible without private keys.

How transactions work on the blockchain

- The owner of a private key creates a new transaction.

- The requested transaction is transmitted to the blockchain network.

- The network's nodes verify the transaction.

- The verified transaction is added to the block.

- The miner calculates and records the block's hash.

- The new block is added to the blockchain.

- The transaction is complete.

Blockchain properties

Due to the operating principles of blockchains, they have several distinctive features.

Security

In traditional databases, information is stored on centralised servers; any centralised database can be compromised by hackers or modified by unscrupulous employees. But that's not the case with blockchain technology. There's no point in changing the information in one block since you'd have to change it in all subsequent blocks since each block contains encrypted data about the contents of the previous blocks. Because all other network participants have their own copies of the blockchain, a different copy would be immediately noticed and recognised as illegitimate. So, in what case will blockchain fail?

For such an attempt to succeed, a hacker must change at least 51% of the blockchain copies, a feat that requires substantial computing resources. While blockchains with fewer participants are vulnerable to this so-called '51% attack', the larger a network gets, the more difficult and costly it is to attempt such an attack. And even if such an attack succeeds, the rest of the network participants would notice the changes and most likely create a new version (a fork) of the blockchain without these changes. Illegitimate transactions are also prevented from being made through the encryption system's use of private keys. That means the blockchain's security isn't based on participants' trust in each other but rather on cryptography and mathematical calculations.

Transparency and anonymity

The transaction history of a blockchain is available to any user, although participants' identity is either anonymous or pseudonymous, depending on the specific blockchain. For example, in the Bitcoin blockchain, participants can see each wallet's balance and its transaction history while personal data remains relatively anonymous.

Immutability

Because the contents of a block can't be changed without changing all subsequent blocks' contents in more than 51% of the blockchain copies on the network, blockchains are very good for storing information. Any validated records are irreversible and can't be tampered with. This means if something is recorded into the blockchain, it stays unchanged there for as long as that specific blockchain network exists.

Blockchain types

Since blockchain technology can be used for different purposes, private and public blockchains are distinguished. Let's get the main types of blockchain easily explained.

- Anyone can join public blockchain networks and mine blocks in them. Bitcoin and Ethereum are prime examples of public blockchains.

- Blockchains with public permissions are open to anyone to join, but certain certified people confirm transactions on them. An example of such a blockchain is EOS.

- Private blockchains are created by specific organisations and used to achieve their goals. They're closed and centralised. They are maintained and controlled by their creators. The data in such a blockchain is not open to everyone. To become a private blockchain member, participants must meet certain requirements, and only certified users can mine new blocks.

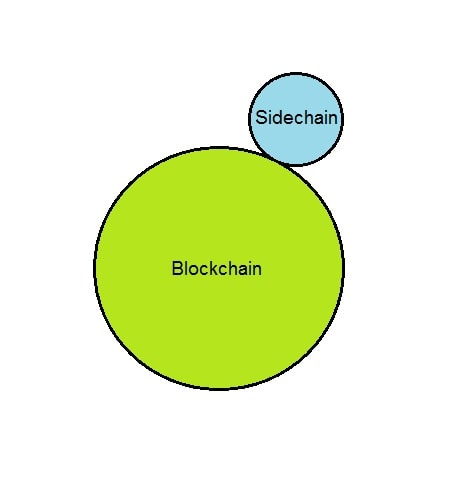

Sidechains

Sidechains are blockchains set up on top of their parent blockchains used to conduct transactions and can act as a bridge between two different blockchains.

This type of blockchain can be used to exchange different cryptocurrencies between users. Another advantage is that the load on the main network is reduced by using an additional blockchain, resulting in faster transactions.

Sidechains are also used for testing and developing products aimed at implementing blockchain technology.

Blockchain advantages and disadvantages

Is blockchain worth it? Let's consider the main pros of the technology, as well as discover why blockchain is bad.

Advantages | Disadvantages |

Security. As mentioned above, hacking and changing information on the blockchain is very difficult. | Scalability. One of the technology's main problems is that blockchain networks currently can't process a large number of transactions in a short period. |

Transparency. Each network participant has access to the blockchain's entire transaction history. | At the time of writing, the size of the Bitcoin blockchain is 317 GB and growing. That means that to keep the network running, each node must have more and more memory to store all the data on the blockchain. |

Privacy. Users' personal data is not available by default. | Transactions on the blockchain network are irreversible. A transaction can't be reversed, even if it was a mistake. |

Immutability and reliability of data. The data on the blockchain network can't be altered or tampered with. | Energy consumption. Blockchain networks using the Proof-of-Work consensus algorithm, such as Bitcoin, consume large amounts of electricity to keep running. |

Protection from censorship. Decentralisation makes it challenging to censor information on a blockchain. | The possibility of a '51% attack'. If a group of users manages to concentrate 51% of all the computing power of a blockchain network in their hands, it will gain control over that network. |

High transaction speed. Since blockchain networks are peer-to-peer, transactions occur directly between users, which greatly reduces the amount of time required to complete a transaction. | |

Low transaction costs. You may ask, "Is blockchain expensive?" Because blockchain networks are peer-to-peer, users don't need to resort to intermediary services to make a transaction. The fees for confirming transactions in blockchain networks are usually lower compared to traditional financial institutions. | |

No downtime. Thanks to decentralisation, blockchain networks work without interruption or days off. | |

Fault tolerance. The blockchain network exists as long as there is at least one node in the world connected to it. |

Blockchain technology applications

The first and most well-known area of blockchain application was cryptocurrencies. However, it wasn't long before blockchain developers realised that this technology could be used for other tasks. Ethereum developers, led by Vitalik Buterin, made a big step forward by implementing the concept of so-called smart contracts. Smart contracts are programmed algorithms that are executed when certain conditions are met.

Let's explore where blockchain technology can be applied (and already is).

- FinTech. Blockchain technology is obviously relevant for cryptocurrency transactions and the entire FinTech industry as a whole. Anything related to transactions can be run on blockchain technology.

- Real estate. The introduction of a distributed ledger into the real estate industry can accelerate buying and selling and give a reliable tool for storing property titles.

- Protection of intellectual property. Blockchain can be used to store copyrights securely, and smart contracts can be used to automate the sale of intellectual property.

- Voting. With the help of blockchain technology, the reliability and accuracy of vote counting can be ensured.

- Logistics. The blockchain can improve the delivery process. Blockchain allows you to eliminate unnecessary intermediaries, minimise the possibility of data fraud and combat counterfeiting.

- Medicine and healthcare. Blockchain technology can be used to create electronic patient medical records, manage medicine supplies, simplify insurance procedures and more.

- Personal identification. Services for identifying and confirming access rights can work on blockchain technology.

- Insurance. A combination of blockchain and smart contracts could revolutionise the insurance industry.

- Other promising industries for blockchain implementation are the Internet of Things, charity, governance, agriculture, energy, gambling, file storage, etc.

Tags

Try our Bitcoin Cloud Miner and get additional crypto rewards based on your trading volume. It's immediately available upon registration.

Try our Bitcoin Cloud Miner and get additional crypto rewards based on your trading volume. It's immediately available upon registration.

FAQ

When did blockchain come out?

In 2008, Nakamoto shared the blockchain source code on SourceForge, inviting software developers worldwide to contribute to the project. In January 2009, the first modern blockchain and the cryptocurrency, Bitcoin, were launched.

Has blockchain ever been hacked?

Several blockchain breaches have occurred on exchanges, which serve as trading platforms for cryptocurrencies. If the security protocols implemented by these exchanges are weak, hackers can gain unauthorised access to sensitive information.

Recently, there has been a significant surge in blockchain hacks as cybercriminals have uncovered exploitable loopholes. Data available to the public indicates that since 2017, these hackers have made away with approximately $2 billion worth of blockchain cryptocurrency. This alarming trend highlights that blockchain technology is not entirely immune to hacking, and users should exercise caution, particularly when trading on exchanges.

Who developed blockchain?

In 2008, there was a significant development in the history of blockchain technology, with the emergence of a research paper titled "Bitcoin: A Peer-to-Peer Electronic Cash System". This paper, which was attributed to Satoshi Nakamoto, appeared in online discussion forums and drew a lot of attention.

Experts note that the blockchain protocol outlined in the Nakamoto research paper is quite similar to the one developed by David Chaum, with the only significant difference being the inclusion of the Bitcoin proof-of-work consensus mechanism for validating data blocks and mining coins. Nevertheless, it is widely believed that Nakamoto is the one who developed blockchain.

Who controls blockchain?

In the case of Bitcoin, the blockchain is decentralised, meaning that no single person or group has control over it. Instead, all users collectively retain control. This decentralisation is what makes blockchain technology so revolutionary. It ensures that no single entity has the power to manipulate the data stored on the blockchain. Additionally, decentralised blockchains are immutable, meaning the data entered is irreversible. For Bitcoin, transactions are permanently recorded and viewable to anyone.

Can I have two blockchain accounts or more?

Unfortunately, no. Only one Blockchain.com Exchange Account can be associated with a verified identity. Only one will be linked to your verified identity if you have multiple accounts. This is the only wallet that you will be able to use for trading.

It's essential to keep in mind that attempting to verify your identity multiple times or for multiple accounts is not allowed. Doing so will result in rejection. Suppose you attempt to verify your identity again while your initial application is still pending or under review. In that case, there may be a delay in processing your initial application, or all applications may be rejected.